Tuesday morning there was big news out of the rail industry: Canadian National Railway (CN) made a stronger offer to acquire the Kansas City Southern (KCS) Railway than what Canadian Pacific (CP) and KCS agreed upon. Whether a deal closes, and between which railways, remains uncertain, but in this edition of The Stockout, I discuss the possible impact that a potential combination between CN and KCS could have on CPG companies.

To sign up for The Stockout, a newsletter focused on CPG supply chains, please click here.

Canadian National made the argument that a CN/KCS transaction would both benefit shippers and shareholders more than a potential CP/KCS deal. The argument that a potential CN/KCS deal would benefit shippers is largely related to extending shippers’ reach into new markets on the railway. While that was the same argument that CP made when it announced its agreement to acquire KCS, CN has a much larger existing network than CP, including reaching into many port cities such as Prince Rupert, Halifax and New Orleans. CN also cited the efficiency that shippers gain from bypassing Chicago (typically the most congested point on the North American rail network) on the CN network (i.e., the bypass that the company gained from its acquisition of the EJ&E railway).

A potential transaction between Canadian National and Kansas City Southern may face greater regulatory scrutiny than a deal between Canadian Pacific and Kansas City Southern. The current standard for receiving regulatory approval for a Class I railroad merger from the Surface Transportation Board (STB has executive oversight of the U.S. Class I railroads) includes demonstrating that a merger would increase competition and be in the public’s best interest.

When I wrote a report for the FreightWaves Passport research on the potential CP/KCS merger, I speculated that the specific CP/KCS business combination might be the only remaining merger option among the remaining Class I railways the STB might approve. There is no network overlap at all between CP and KCS and in no cases did the number of railways in competition decline from three railroads to two, or from two to one. In fact, the railways said that, in a few select cases, the number of railroads in competition might increase from two to three as a result of the merger.

In contrast, while CN and KCS have little direct overlap (CN said Tuesday that the only customer overlap is about five customers serving about nine plants), the two railways both have parallel north-south mainlines that can take customers from, for instance, the Gulf Coast to Chicago, the largest North American freight rail hub. At least on the surface, that raises questions as to whether railway competition will decline in north-south freight corridors. For its part, CN indicated that it believes that potential regulatory concerns over network overlap and a potential reduction in competition can be made up for through mitigation actions, which the company has been required to perform following past acquisitions.

Around 120 domestic loaded containers moved outbound from Laredo in the past week. CN says that it would rather not pick up freight in Laredo, but rather, from deep inside of Mexico, which a potential acquisition of KCS would enable.

The charts from left to right show outbound domestic loaded container volume from Laredo, door-to-door domestic intermodal spot rates from Laredo to Chicago and the Laredo Headhaul Index, which is the difference between outbound and inbound truckload demand. (Source: SONAR)

To learn more about FreightWaves SONAR, click here

So what does this mean for CPG companies? CN stressed that most of the synergies anticipated from acquiring KCS are revenue synergies and, within the category of revenue synergies, the bulk of the anticipated synergies come in the intermodal segment. The concept is that the combined company would have longer corridors under its control so it can invest in the broader intermodal network to support that growth while also avoiding interchanges and border crossings that impair intermodal efficiency and service. The more efficient, faster and consistent an intermodal network becomes (as intermodal service becomes “truck-like”), the more effectively intermodal provides shippers with savings when compared to truckload.

When CP discussed its pending acquisition of KCS, some of the specific examples of taking trucks off the road were in the Chicago-Dallas corridor, a busy lane for truck traffic where rail intermodal is being underutilized. In contrast, CN’s intermodal comments Tuesday morning suggest that the expanded intermodal reach could be broader than what CP discussed and in lanes that are not traditional intermodal lanes, including many cross-border lanes.

CPG companies moving freight that does not need to be refrigerated are often good candidates to utilize domestic intermodal. General Mills is an example of a CPG company that utilizes domestic intermodal; the long-haul nature of many of its moves and the lack of refrigeration needed for many of its products makes intermodal ideal. In addition, CPG companies are often among the categories of intermodal shippers that are most concerned with the sustainability of their supply chains. In addition to often undercutting truckload costs by 10%-15%, the intermodal fuel surcharge is typically half of the truckload fuel surcharge.

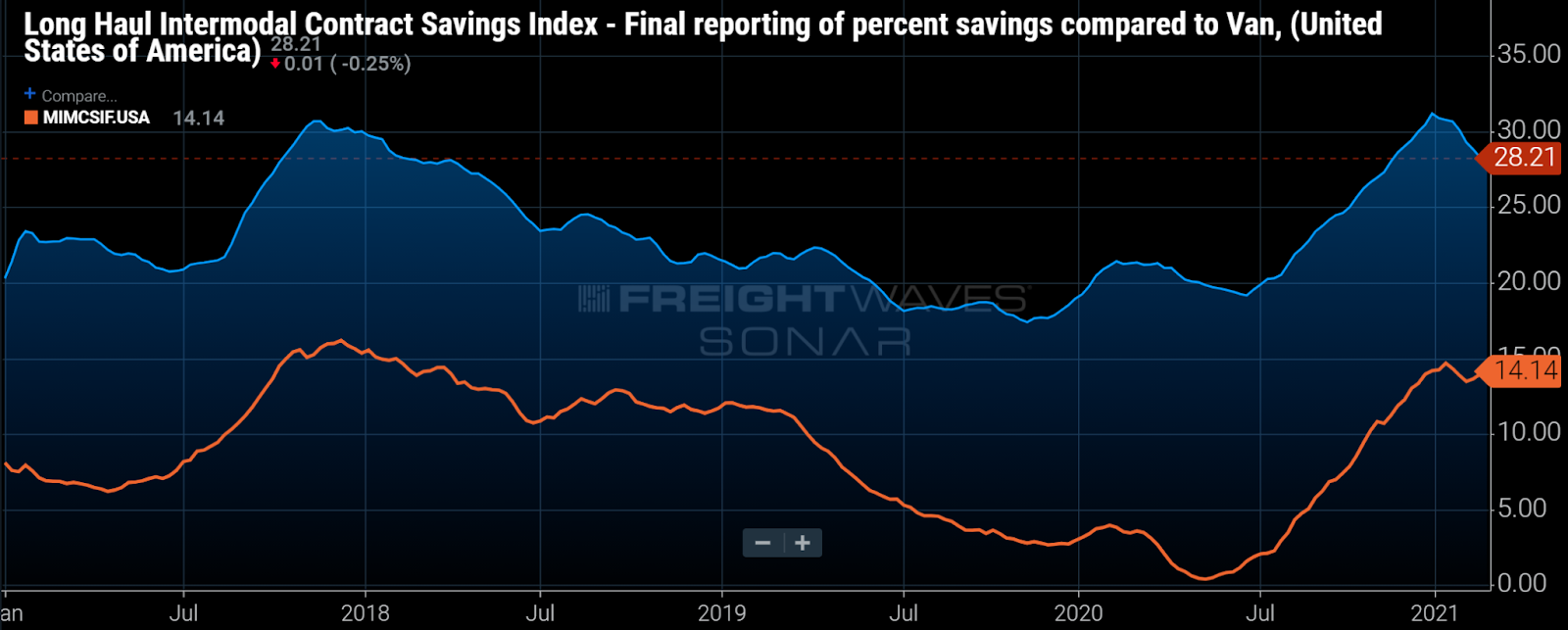

Shippers’ savings on intermodal contracts, relative to truckload, increase with longer lengths of haul; additional long-haul intermodal lanes may become economically viable to a wider range of shippers if KCS is acquired by CN or CP.

Average intermodal contract savings, relative to truckload contracts, for long haul (>1,200 miles) and medium haul (800-1,200 miles) loads are shown in blue and orange, respectively. (Source: SONAR)

To learn more about FreightWaves SONAR, click here

Elsewhere this week, highlighting recovery from the pandemic, Coca-Cola’s volume in March 2021 was back to pre-pandemic March 2019 levels. That represented a milestone for the company, which has had sales greatly negatively impacted, on a net basis, by consumers spending more time at home. While the company has been gaining share in both at-home and outside-the-home segments during the pandemic, Coca-Cola enjoys higher market share in the outside-the-home segment, so it loses sales overall when consumers are less mobile. The company’s sales in March in the outside-the-home segment were still negative when compared to March 2019, but declines in that segment have moderated and were fully offset by positive volume in the in-home segment when compared to 2019. Companywide, the company expects its earnings this year to be around 2019 levels.

The impact that higher input costs may have on Coca-Cola’s financials may be more of a 2022 event rather than a 2021 event. Similar in many ways to what Pepsi said last week, Coca-Cola’s input costs are fairly well hedged near term. That is part of why the company was able to maintain its 2021 guidance when it reported Monday in the face of widespread ingredient cost pressure that has mounted in recent months.

To receive The Stockout, CPG-focused newsletter, please click here.