The relative weakness in diesel prices four weeks into the start of the IMO 2020 regulations does not surprise Marathon Petroleum CEO Gary Henninger.

Henniger, on a conference call with analysts after the release of the company’s fourth-quarter earnings, said the independent refiner did not expect in the first weeks of the new year “to see an acceleration of distillate prices.”

“This will be stair-stepped into the year and that’s still how we feel,” he said.

Marathon operates 16 refineries with capacity of 3 million barrels a day and is considered the nation’s largest independent refiner following its acquisition last year of Andeavor, which had been known for years as Tesoro.

The fact that diesel prices have not strengthened relative to crude — and in fact, have declined — has not thrown a wrench into Marathon’s initial analysis of the way the rollout of IMO 2020 would take place, Henninger said. The first strategy of Marathon was to wait for the collapse of the price of high sulfur fuel oil (HSFO), which is the product that had been the primary fuel for propelling ships. But its sulfur content of 3.5% is far more than the IMO 2020 regulation of 0.5%, and its price has slid.

On Sept. 23, the price of the new compliant fuel, known as very low sulfur fuel oil (VLSFO), in the key shipping port of Fujairah, United Arab Emirates, was approximately $487 per metric ton, according to S&P Global Platts. The price of HSFO on that date was just under $417. The prices more recently were $565 and $312, respectively.

That widening of the spread, according to Heninger, has allowed Marathon to either eliminate the production of HSFO in its refineries wherever it can by using its coking capacity — which can turn heavier feedstocks into lighter products — or by buying HSFO to put into cokers, mostly in its U.S. West Coast refineries.

“We were looking first at feedstocks being depressed, giving us higher margins,” Henninger said. “That is happening.”

But as far as the price of diesel, Henninger added, “We were conservative. We did not expect a significant run-up in crack spreads.”

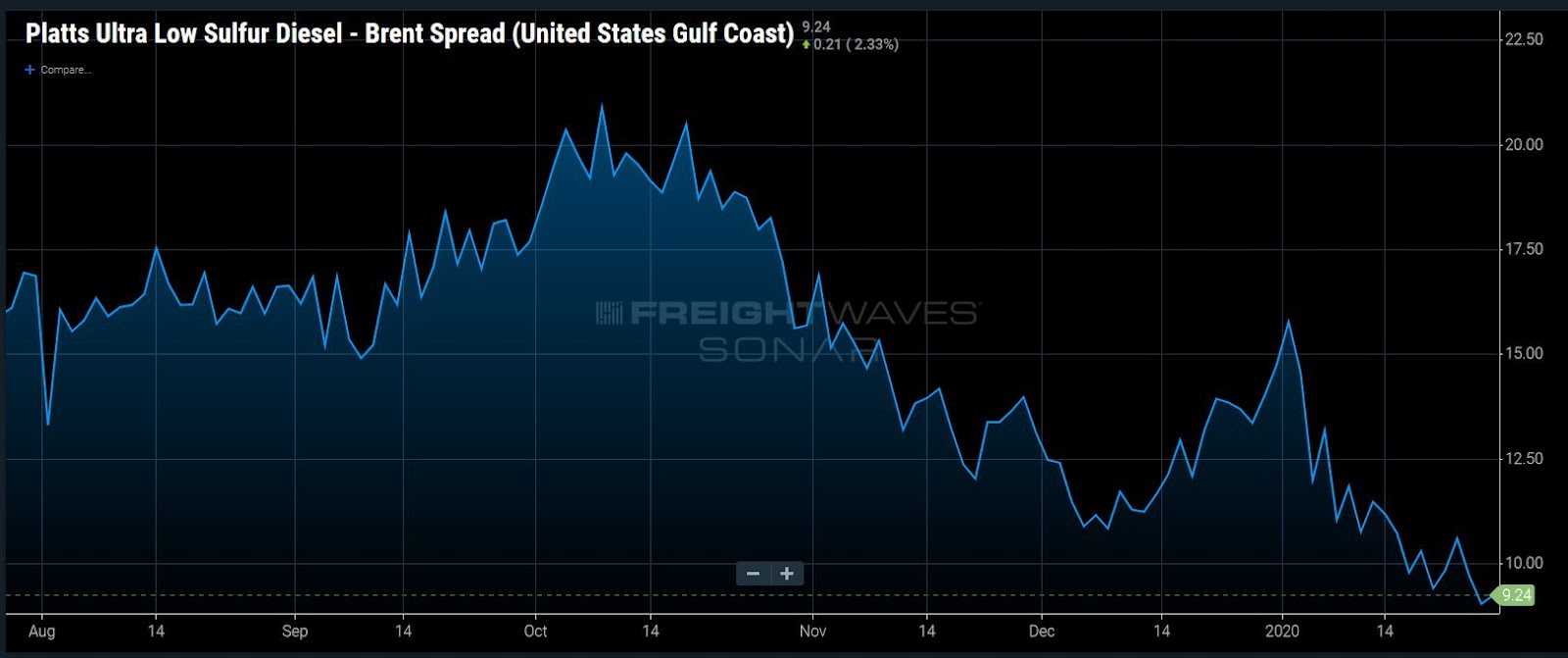

The spread between Brent crude and diesel did move up significantly in October, and some observers believed that was probably a sign of the market getting ready for IMO 2020. But it has fallen since then with a particularly sharp decline in recent weeks, fueled in part by the coronavirus and the expectation that will crater jet fuel demand. Jet fuel, like diesel, is a distillate, and a drop in jet would be expected to spill over into diesel.

According to data from S&P Global Platts, the spread between U.S. Gulf Coast diesel and dated Brent exceeded $20 per barrel for a few days in early October. It’s now less than $10.

But Henninger said he expected those diesel crack spreads to widen. A significant refinery maintenance season is coming up worldwide in March and April, he said, with about 8 million barrels per day offline — a large amount. “That will put a draw on not only gasoline but also diesel inventories,” he said.

He said he’s also encouraged by the level of ship compliance with IMO 2020. The more compliance, the more diesel-related products the industry will need to consume.

VLSFO is a product that is largely made by blending an intermediate product called vacuum gasoil (VGO). In a refinery, VGO previously could be put into a cat cracker to make gasoline and some diesel, or be put into a hydrocracker to make just distillate products like diesel.

One theory of how IMO 2020 would play out was that VGO would be diverted away from cat crackers and instead used to make more diesel or VLSFO. According to Ray Broooks, executive vice president of refining, at Marathon that’s what is happening. He said in the company’s Gulf Coast operations, Marathon has taken about 40,000 to 50,000 barrels per day of VGO away from cat crackers and instead used them to make VLSFO. “We’ve seen a very, very strong VGO market and so we pivoted on that,” Brooks said.

The response to that diversion had been seen by some analysts as a move that would eventually tighten gasoline supplies and boost the price of gasoline, encouraging the move of VGO back into the cat cracker. But the world is awash in gasoline and for now, there is no sign of that occurring.