Knight-Swift (NYSE: KNX) warned in late December that its earnings per share for the fourth quarter were going to slip into the range of 50 cents to 52 cents per share. When the earnings came out Wednesday, the company beat that estimate.

The earnings-per-share figure was 55 cents, but it still is down from the 62-65 cents per share guidance that had been in effect until the late December announcement.

Beyond that, the report of the company featured pretty much everything one might expect from a truckload carrier navigating the difficult market of 2019. The operating ratio (OR) of the truckload segment weakened to 87.8% from 83.3% in the fourth quarter of 2018. The adjusted OR was 86.2% versus 80.9%. Revenue for that segment fell 11.2%, to $861.4 million, while operating income dropped to $118.3 million, a decline of 35.4%.

For the full year, the OR under generally accepted accounting principles (GAAP) was 88.1% versus 87.2% in 2018.

The company’s logistics segment saw its OR weaken to 93% from 89.4% in 4Q2018, while the brokerage-only gross margin dropped to 15.5% from 18.3% in the corresponding quarter of 2019. The division’s revenue was down 30.2% to $92.7 million, while its operating income dropped 55.7% to $5.87 million.

The intermodal division barely broke even. It had operating income of $600,000, a decline of 95.4%, while revenue dropped 18.7% to $111.8 million. That narrow operating profit meant an OR just under 100% at 99.5%.

But despite the poor report, Knight-Swift stock was up more than 5% at approximately 11 a.m. Wednesday. That appears to be primarily because Knight-Swift said in its earnings release that its guidance for full year 2020 was $2 to $2.15 per share. One consensus estimate of Knight-Swift’s earnings for the year put it at $2.03 per share, so a range that climbs to $2.15 would mark a significant improvement.

“KNX shares are outperforming today following the release of 4Q results and inaugural 2020 EPS guidance,” the team led by Amit Mehotra at Deutsche Bank said in a comment Wednesday morning. “The details in the Q were a bit better: notably trucking OR of 86.2% despite significant utilization and pricing headwinds (both down 6% yoy). And this appears to be dragged down by weaker-than-expected KNX truckload OR of 88.2% … which will most likely snap back materially when truckload fundamentals improve.”

The Deutsche team said the earnings forecast that appears to have kicked the stock price higher was actually to be expected. “Both near-term 1Q guidance (35-38c) and the 2020 forecast ($2-2.15) were within expectations (despite the full-year tax rate being a bit higher) … with mgmt. still calling for an inflection in earnings power in 2H,” they wrote.

The earnings release from Knight-Swift had a summary of the tough environment the company faced. “While the truckload freight environment remains competitive, evidence of capacity rationalization is mounting, including impacts from trucking company business failures, lower Class 8 new truck orders, further weakening of Class 8 used tractor values, growing Class 8 used inventories and contraction in trucking employment,” the statement said.

But turning to the rest of the year, Knight-Swift management was more optimistic. “Capacity rationalization may further accelerate given the mild freight seasonality that is typical in the first quarter, significant insurance cost inflation and the new regulatory introduction of the CDL Drug & Alcohol Clearinghouse, which we believe will foster a more favorable freight environment in the second half of 2020,” they wrote.

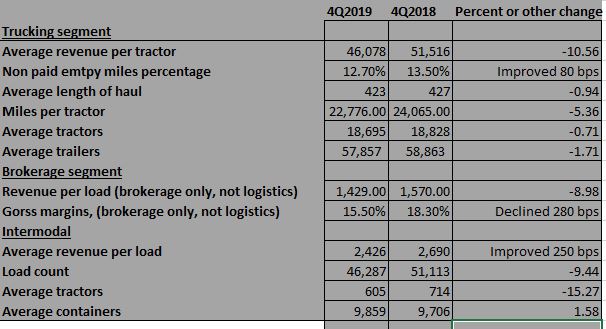

Virtually all the trucking metrics were negative compared to the fourth quarter of 2018. Average revenue per tractor was down 10.6% to $46,078. The nonpaid empty miles actually improved to 12.7% from 13.5%. The average length of haul was also up slightly, 1.2% to 423 miles. But miles per tractor were down 5.4% to 22,776; average number of tractors dropped 0.7% to 18,695; and average number of trailers was down 1.7% to 57,857.

In the brokerage division, revenue per load was down 9% to $1,429 and the gross margin declined 280 bps to 15.5%.

The numbers in intermodal were particularly gruesome. Average revenue per load was down 10.2% to $2,416 and the load count dropped 9.4% to 46,287.